Private health insurance - a matter of life and death?

Carly McKenna

Going private - do I need it right now?

A lot of people would have you believe that private health insurance is a necessity – but in Australia, the reality is that we’re lucky enough to have a fantastic (and free) public health system. If you end up in an accident or emergency, you can access a high level of care regardless of whether you have private hospital cover (although this doesn’t account for any potential ambulance cover!).

That doesn’t mean you should dismiss the idea. In fact, private health insurance has some key advantages, particularly during a health crisis like this.Taking out private health insurance has many benefits (protection against the unexpected, proactive health and wellbeing benefits etc.), eases pressure on our public health system and in some cases, even saves you money!

In this topic, we’ll explain:

- When and why it’s worth taking out private health insurance

- What you need to know about the essentials (and extras)

- How you can get the most value out of your cover

Ready? Let’s go.

Paying for the protection, when is the right time?

When you’re young, healthy and already getting free health care, it may seem that there isn’t much value in private health insurance. However the government offers a few big financial incentives for younger people to purchase private health insurance, in an effort to make it more sustainable.

Financial wins aside, there are a bunch of reasons to jump on private health insurance when you’re young, including ambulance cover for accidents, dental up-keep, physio and proactive health care to prevent any issues before they arise.

If you fall into one of the following categories, it may be time to start considering your options.

Earning over $90,000? Avoid the Medicare Levy Surcharge

In Australia, the Medicare levy on your income (calculated when you lodge your tax return) helps fund our public health care system. If you’re earning below $90,000 a year, this levy will be 2% of your taxable income. However, once you start earning above this threshold, you’ll have to pay a Medicare Levy Surcharge (MLS) that can be anywhere from 1-1.5%, depending on how much you’re earning. That’s a minimum of $900 extra that you’ll be paying each year.

Enter private health insurance! If you have private hospital cover, you won’t have to pay the surcharge come tax time (and if you take out private hospital cover part way through the financial year, the surcharge will be calculated on a pro rata basis). There are plenty of basic hospital policies that cost less than $900, which means that taking out basic cover can actually save you money if you’re earning over $90,000!

Approaching 31? Avoid Lifetime Health Cover loading

Lifetime Health Cover (LHC) loading is another big incentive for taking out private health insurance early. If you don’t have private hospital cover before you turn 31 (and you decide to take it out later), you’ll pay an extra 2% on your premiums for every year that you wait. Ouch!

Keep in mind that if you never get private health insurance, the LHC loading will never affect you. But if you’re approaching 31, you may want to start thinking ahead so that you don’t end up paying more down the track.

We should note that loading applies to hospital coverage only (not extras or standalone ambulance cover) and is not reduced by the government rebate (if applicable). The maximum loading is 70% and if you’re in it for the long haul, once you’ve paid for 10 continuous years the loading is removed.

Earning less than $90,000? Save up to 25% on premiums

In addition to avoiding surcharges, taking out private health insurance early can help you save money on your premiums.

The private health insurance rebate is an amount that the government contributes towards the cost of your private health insurance premiums, depending on your income.

If you’re earning less than $90,000 per year, you’ll receive the highest rebate percentage, which is more than 25%! Once you’re earning over $90,000, the rebate will drop to 16.7% – and it will continue to decrease as your income increases.

Aged 18 – 29? Save an additional 10%

Insurers now have the option to offer additional discounts to new customers who sign up before they turn 30. These discounts work out to be 2% for each year that you’re under 30, with a maximum discount of 10%. Once you have an age-based discount on your policy, you’ll also retain that rate until you turn 41.

This means that if you’re 25 and decide to take out private hospital cover for the first time, you’ll receive a 10% discount on your insurance premiums for the next 16 years. Not bad!

Essentials and extras explained

If you’ve decided that it’s time to take out health insurance, the next step is figuring out what kind of health insurance you’ll need (and what you’ll actually get value out of). There are two types of cover that you should know about:

- hospital cover

- extras cover

Hospital cover

Hospital cover helps provide peace of mind for the unexpected and covers the costs of medical treatment when you go to hospital as a private patient. It usually means you can choose your doctor, your preferred hospital and the timing of your procedure (subject to availability). Given the wait for a procedure on the public system can sometimes be over 2 years (particularly in crisis situations like right now), private health insurance can help you get treated more promptly. It also means ambulance costs are covered if there is an emergency.

When we talk about private health insurance, hospital cover is usually what we’re referring to.

Keep in mind you will usually need to serve a waiting period before you can claim for hospital cover. Waiting periods prevent people from taking out health insurance, making a high-cost claim and then cancelling their policy. Although they can be frustrating, waiting periods protect existing members from having to bear these costs.

Waiting periods will often vary, but the maximum waiting periods for hospital cover (set by the government) are:

- 12 months for the treatment of pre-existing conditions (that is, any condition that you had signs or symptoms of in the six months before you took out cover)

- 12 months for pregnancy-related services

- 2 months for psychiatric care, rehabilitation, palliative care and any new health conditions that require hospitalisation.

Extras cover

Extras cover is designed to help you stay healthy and a means to cover planned or unplanned treatment that would otherwise be very costly without an extras policy! For example, if you visit the dentist or have ongoing physio sessions, and you have the right level of extras cover, you’ll usually be able to claim part of the cost back (rather than being out-of-pocket for the whole amount). The most common categories of extras include:

- Dental (general and major)

- Orthodontics

- Optical

- Clinical therapies (like physiotherapy and chiropractic)

Extras cover isn't really ‘insurance’ (in the traditional sense of covering you for an emergency) because you usually know when you're going to need a dental check up or a new pair of glasses. However, taking out extras cover can help you budget for these things and reduce your out-of-pocket expenses. The trick is to make sure that you’re claiming more in benefits than what you’re paying on your premiums.

When it comes to extras, there are a few things you’ll need to keep an eye out for:

- Annual limits and item limits – The amount you can claim back will usually be restricted, based on an annual limit and an item limit (for each visit). Watch out for item limits! A $400 annual limit for physiotherapy may sound like a great deal, but if you can only claim a set benefit of $40 per visit, it will take ten visits to claim your annual limit

- Waiting periods – You’ll generally need to get past a waiting period before you can start claiming benefits – and for services like major dental, that can mean a 12 month wait! Extras waiting periods can vary significantly between insurers, so make sure you check your policy!

Although many policies will include both hospital and extras cover, you don’t need to purchase both types (and you can even choose to go with different insurers for each). Just keep in mind that if you’re looking to avoid the MLS or the LHC loading (those financial incentives we talked about earlier), you’ll need hospital cover as a minimum – extras cover alone won’t cut it!

Cover that won’t cost you an arm and a leg

Not all health insurance policies are created equal and the best deal will depend on what you want from your policy. Do you just want to avoid the surcharges at tax time and save yourself money, or are you looking to maximise value from your extras?

We’ve done the research for you and broken down our recommendations into two categories:

Price is Right

As of April 2020 insurers are required to classify their private hospital cover into four tiers: Gold, Silver, Bronze or Basic. These tiers make it easier to compare policies so you know what you’re getting when you choose a policy in a particular tier. However, while these tiers determine the minimum standard categories of treatment, health insurers can and do sometimes add additional coverage at their discretion. You can read more about what’s included in each category here.

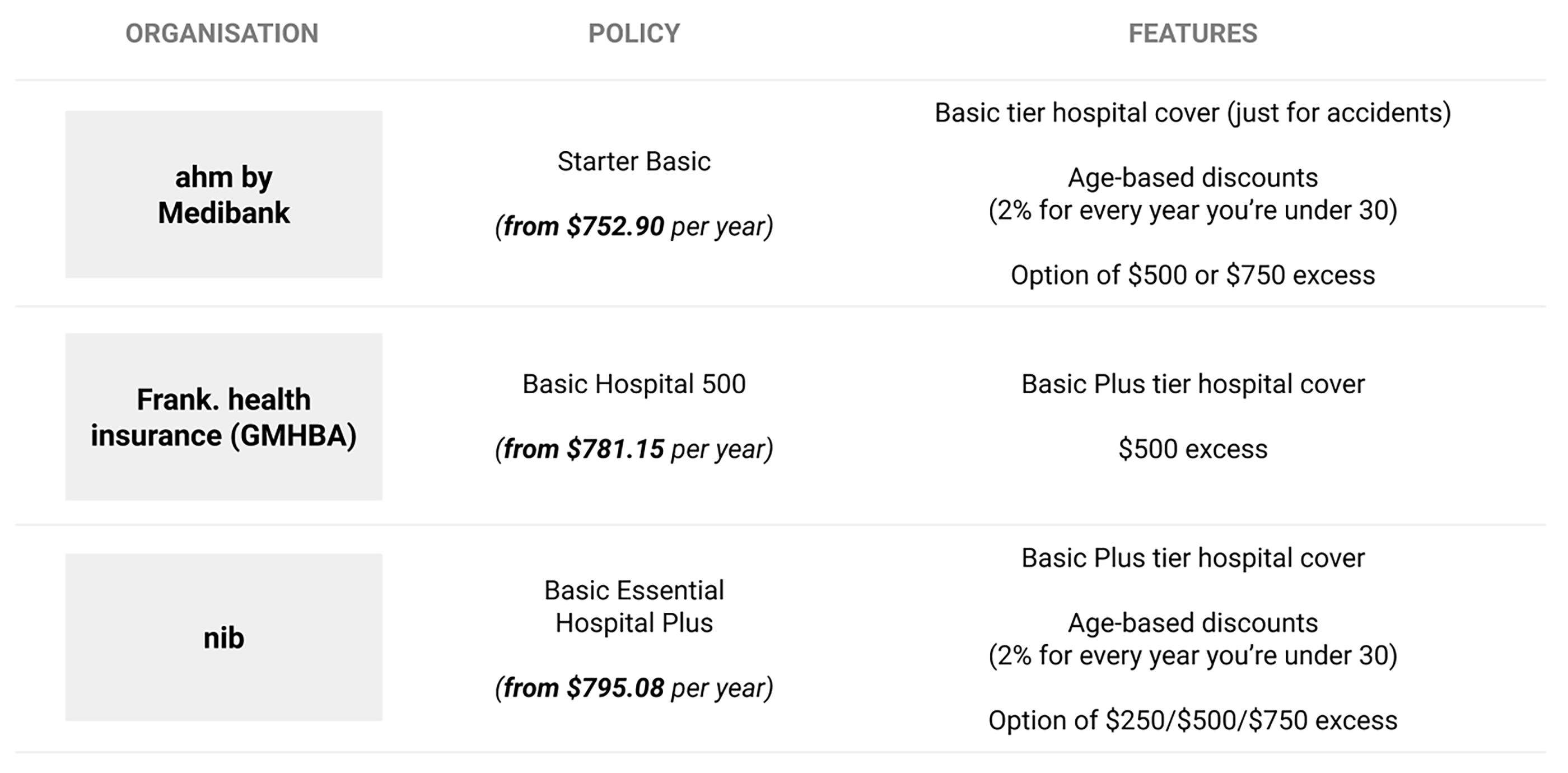

If you’re earning over $90,000 and want to avoid the Medicare Levy Surcharge, we suggest going with a Basic level of hospital cover that costs less than $900. Basic policies offer the lowest tier of cover at the lowest price point (that’s palliative care, rehabilitation and psychiatric care; likely under restricted cover), so they’re good for saving on tax. Just don’t rely on them if you’re after comprehensive health cover! Although they may cover treatment after an accident, they often don’t include follow-up care. You’ll also remain on public hospital waiting lists and usually receive the same treatment as public patients.

Frank, nib and ahm (Medibank) all offer the cheapest policies in this tier. However, the exact price of your policy will depend on factors such as your age, your income and what state you’re in – so make sure you get a couple of quotes to see who will save you the most.

More than Money

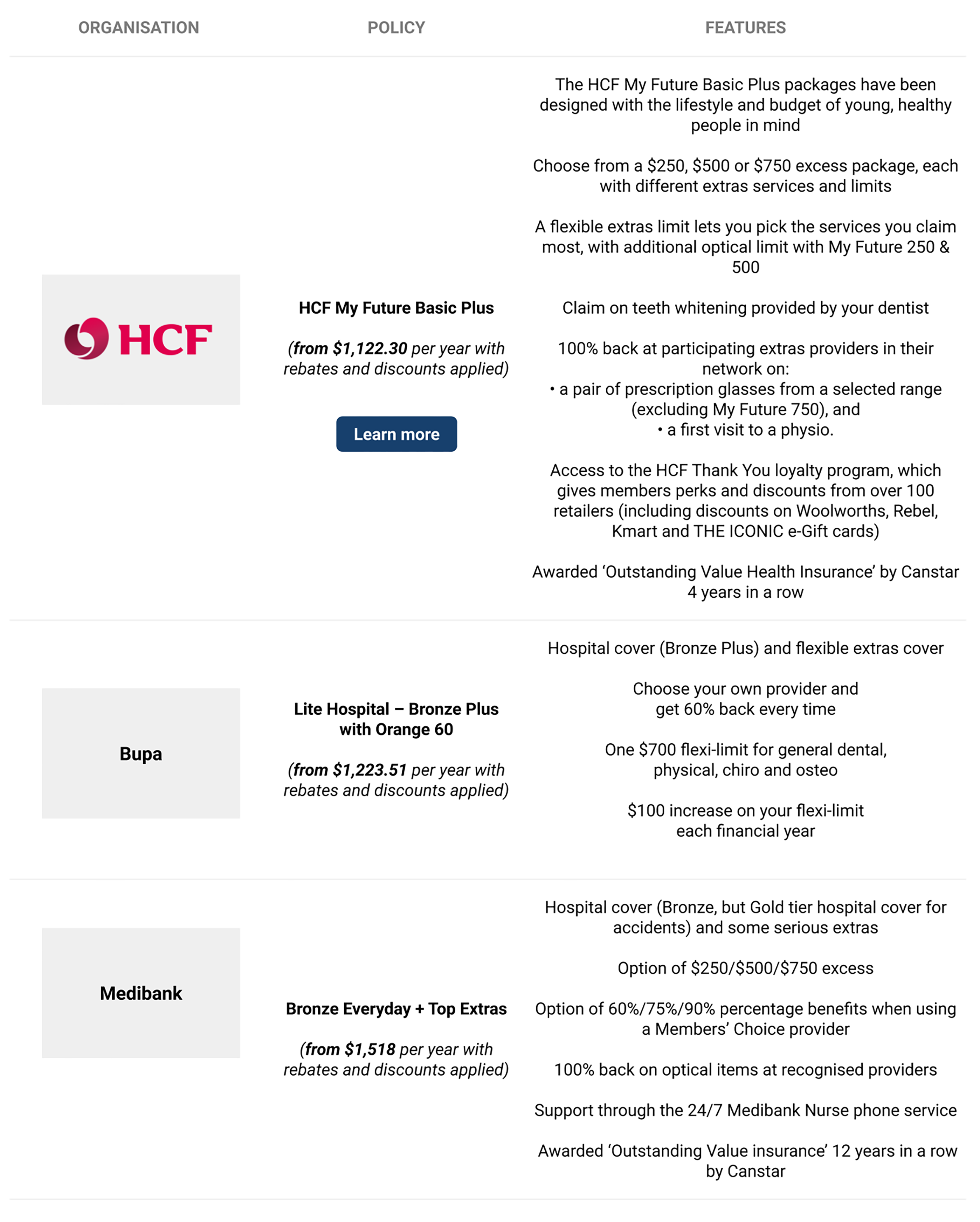

If you’re looking for comprehensive cover from your health insurance, HCF, Bupa and Medibank offer affordable options combining hospital cover with great value extras.

As Australia’s largest not-for-profit health fund, HCF put people before profit. That means they put their members’ health before anything else. HCF is a great choice with three packages designed specifically for young people, offering a flexible extras limit to give you freedom on how you use your extras.

Bupa is another great choice. They offer flexible extras cover, with a flexi-limit that lets you choose how you use your annual limit, and your flexi-limit will increase with each year that you’re with them (on included services only).

When it comes to item limits, Bupa and Medibank also offer great percentage benefits with these policies (60%, 70% and 90%). These will usually work out better for you than set benefits (like $60 per visit), and if you’re spending more on your services, you’ll get more back!

Thinking of taking out health cover? Here’s why to choose HCF

When it comes to healthcare, people want to know they’ll be genuinely cared for in their time of need. There’s care – and then there’s Uncommon Care.

Why? Because as Australia’s largest not-for-profit health fund, our members are at the heart of everything we do. We put the health and wellbeing of the 1.6 million Aussies we cover before anything else.

Why HCF?

- You can count on us, we’re Australia's most-trusted health fund 2 years in a row*.

- We’ve gone above and beyond to develop holistic mental health and wellbeing programs with access to a range of options that work, and the freedom to choose which is right for you^.

- We’re supporting your health needs with access to telehealth services, like physio, psychology or dietetics, from HCF-recognised providers, for eligible members until 31 December 2020.

- You can take full control of your health cover with the HCF My Membership app.

- You’ll have a 30-day cooling-off period because we want you to be happy with the health cover you’ve chosen.

* Roy Morgan Net Trust Survey 2018 and 2019.

^ Available with HCF-contracted providers, subject to your location and your hospital cover. Waiting periods apply

That covers it!

Like we’ve said, private health insurance definitely isn’t a necessity, but taking it out when the time is right can actually save you money in the long run. Keep our tips in mind and you’ll be able to make the most of your cover (without it costing you an arm and a leg).

Stay tuned for upcoming topics or check out or other useful articles here. We’ve got plenty more gold to help you make the leap from top student to top professional!

Got feedback? We’d love to hear from you! Shoot us an email at [email protected]

Author by-line

Not signed up to The Launchpad yet?

Subscribe below to get the full experience!

Disclaimer: The information provided in this article is general in nature only and does not constitute personal advice.

The information has been prepared without taking into account your personal objectives, financial situation or needs.